The energy transition is often described as a path driven by electrification, renewables and efficiency. In the technical debate, the focus is on performance, efficiency, system architecture and energy availability. However, less attention is paid to the material basis of this transformation: the critical minerals and metals needed to build electric motors, drives, batteries, networks and infrastructure. It is precisely at this level that a new area of industrial vulnerability is emerging, linked to the geographical concentration of raw materials and refining capacities. The picture that emerges from the 7th MED & Italian Energy Report, recently presented by SRM (Intesa Sanpaolo) and ESL@Energycenter (Politecnico Torino), highlights how the security of electrification depends not only on the kWh produced, but also on the stability of the supply chains for strategic materials.

Critical raw materials: concentrated reserves

The spread of electrical technologies — high-efficiency motors, storage systems, electric traction, networks — is leading to a structural increase in demand for critical raw materials (CRMs). These materials are essential for permanent magnets, windings, power electronic components, batteries and conversion systems.

The report emphasises that the transition to an electrified energy system will lead to a very significant increase in demand for these resources, opening up a new front in energy security: technological and material security. It is no longer just a question of fuel or electricity supply, but also of reliable access to the minerals and semi-finished products needed to build the technologies.

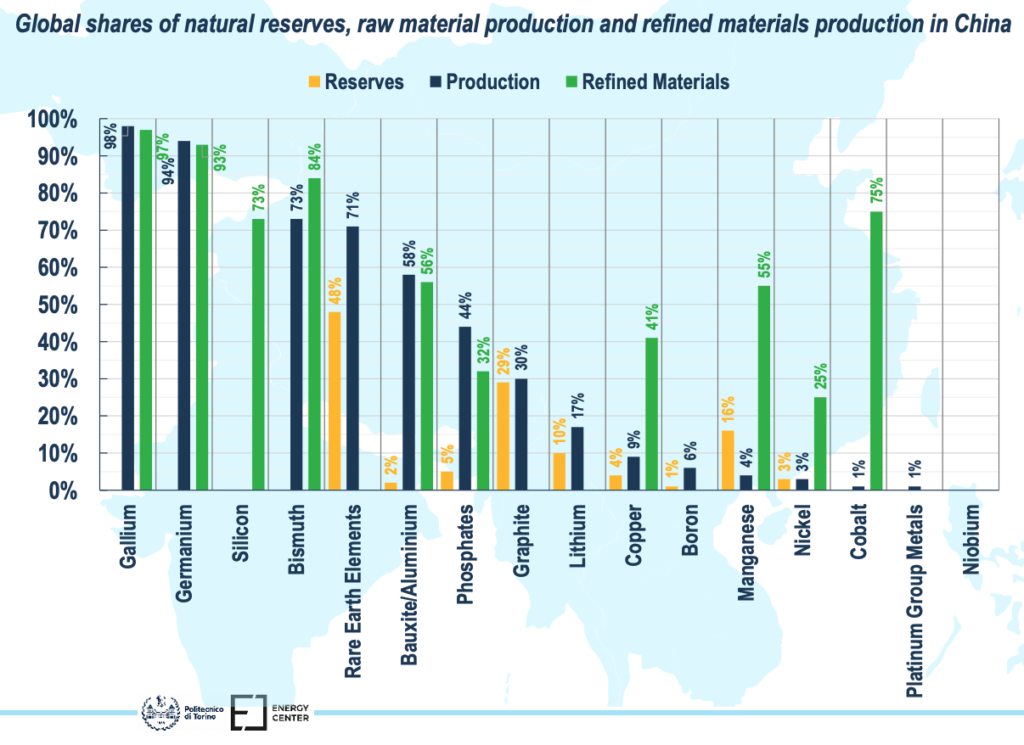

Critical raw materials are, in fact, distributed among a very limited number of countries, mostly outside the Mediterranean basin and Europe, with particularly high levels of concentration. According to the report, China holds dominant shares of production for many strategic materials: approximately 71% of rare earths,76% of tungsten,67% of graphite,64% of magnesium and 68% of vanadium worldwide. Other key materials show similar concentrations: the Democratic Republic of Congo accounts for around 70% of global cobalt production, while Brazil supplies 93% of niobium. Even where significant reserves exist in other countries, such as phosphates in Morocco, accounting for68% of global reserves, China remains the leading producer, accounting for approximately44% of production. This higly polarised structure has a direct impact on the security of technology supply chains linked to electrification.

The issue of refining and intermediate processing

This concentration affects not only extraction but also the refining and intermediate processing of materials. The data reported in the report indicate that between 2020 and 2024, approximately 90% of the growth in the global supply of refined critical materials was guaranteed by a single leading country for each supply chain: Indonesia for nickel and China for cobalt, graphite, and rare earths. In the specific case of cobalt, China controls approximately 78% of global refining capacity. On the extraction side, the Democratic Republic of Congo accounts for over 80% of global cobalt exports, while China maintains production shares of 71% for rare earths, 67% for graphite and 64% for magnesium. Supply growth is therefore not widespread but driven by a few industrial hubs, with a supply chain that remains highly polarised in the stages with the highest added value. This structure increases exposure to supply shocks and price volatility, with possible knock-on effects on industrial competitiveness, investment planning and cost stability. For manufacturers of motors and electromechanical components, this translates into greater uncertainty regarding both material prices and delivery times.

Rapidly growing global demand

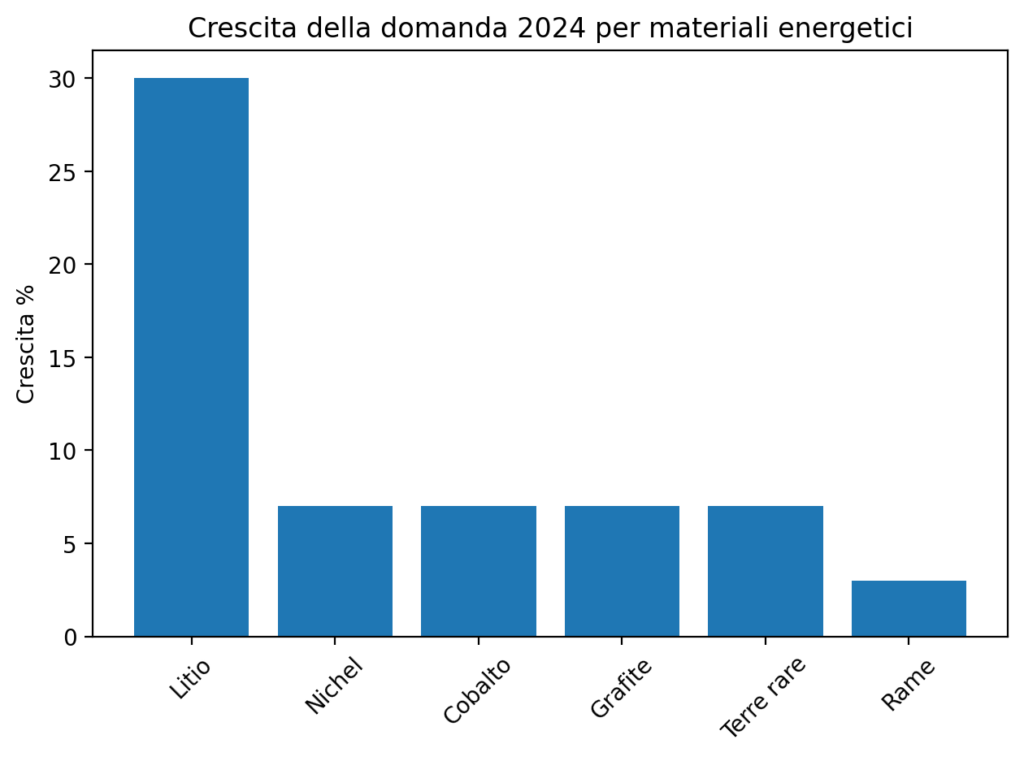

Demand dynamics further reinforce the risk picture. According to estimates cited in the report — based on analyses by the IEA (International Energy Agency) and UNCTAD (United Nations Conference on Trade and Development) — demand for minerals for the energy transition is expected to almost triple by 2030 and more than quadruple by 2040. The most intense growth is expected between 2025 and 2035. Some signs are already visible in the latest data: in 2024, demand for lithium grew by around 30%, while nickel, cobalt, graphite and rare earths recorded increases of between 6% and 8%. These are materials directly or indirectly linked to electrical technologies and energy conversion. For the world of electric motors, this scenario points to growing pressure on supply chains and greater exposure to price volatility.

Import dependency and regulatory response

For the European and Mediterranean area, the document highlights an almost total dependence on imports of numerous critical raw materials. This entails not only industrial security risks but also trade balance implications, which is already in deficit for trade in materials with countries outside the area. In response, the European framework has introduced domestic development targets for extraction, processing and recycling, as well as limits on the concentration of imports from a single supplier. These are strategic guidelines aimed at reducing extreme dependence and improving the resilience of supply chains, albeit with necessarily long implementation times.

The role of recycling and new design choices

Another strategic element concerns the recycling of critical materials. The report highlights the growing contribution of recycled materials, for example, cobalt, to meeting demand. Although not a complete solution in the short term, recycling represents a technical and industrial lever for alleviating pressure on primary supply chains. For manufacturers of electric motors and systems, this issue translates into greater attention to end-of-life design, material recoverability and component circularity.

Overall, the technical message is clear: electrification does not eliminate dependencies; it transforms them. Dependence on fuels is accompanied by dependence on critical materials. For the electric motor sector, traditionally focused on efficiency, power density and reliability, a new system variable comes into play: the resilience of the material supply chain. Integrating this factor into design and strategic choices becomes an integral part of medium-term industrial competitiveness and the stability of electromechanical supply chains.

Lithium

Use: batteries for electric vehicles and storage systems.

Demand in 2024: +30% year-on-year.

Production and refining: approximately 70–80% of recent growth in refined production is concentrated in China; new mining growth also from Argentina and Zimbabwe. Prices have fallen by more than 80% from their 2022–2023 peak despite strong demand growth.

Nickel

Use: batteries (high-nickel chemistry), alloys for electrical and industrial components.

Demand in 2024: +6–8%.

Production and refining: Indonesia is the leading growth centre for refined supply and accounted for around 90% of the increase in refined production between 2020 and 2024. The share of the top three countries in refining rose from 60% to 80% between 2020 and 2024.

Cobalt

Use: cathode materials for batteries, superalloys.

Demand in 2024: +6–8%.

Production: The Democratic Republic of Congo accounts for around 70% of global mining production and over 80% of exports.

Refining: over three-quarters of global refined output is concentrated in China. The share of the leading producer rose from 68% to 78% between 2020 and 2024.

Graphite (natural and synthetic)

Use: battery anodes, electrochemical components.

Demand in 2024: +6–8%.

Refining: China produces over 95% of battery-grade graphite and dominates the processing chain. Around two-thirds of the growth in battery recycling capacity is also located in China.

Copper

Use: electric motor windings, cables, networks, transformers, renewables.

Demand in 2024: +3%. Growth is mainly driven by investments in electricity grids.

Production: less concentrated than battery metals, but with a risk of deficit: the scenarios indicate a possible supply gap of around 30% by 2035 due to declining ore grades, long development times and rising costs.

Rare earths element (magnetic applications)

Use: permanent magnets for high power density electric motors and wind generators.

Demand in 2024: +6–8%.

Production and refining: China accounts for around 70% of production and over 95% of the refining of magnet materials. The rest of refined production is fragmented; a single non-Chinese operator accounts for around 4% of global production.

Manganese

Use: battery chemicals and special alloys.

Demand: growing with manganese-rich battery chemistries

Refining: China produces approximately 95% of high-purity manganese sulphate for batteries, currently one of the emerging bottlenecks.

Concentration indicator

Between 2020 and 2024, the share of the top three countries in the refining of key energy minerals rose on average from 82% to 86%. In many cases, around 90% of the growth in refined supply came from the top single supplier country. This level of concentration is considered one of the main risk factors for the electric motor, battery and network supply chains.

(Source: IEA, Global Critical Minerals Outlook 2025)

{kind=link}