As some analysts correct their outlook on copper forecasting an increase in average prices, duty tariffs still represent a source of uncertainty and controversy. Furthermore, according to studies, they are unlikely to boost domestic production in the United States and reduce reliance on imports.

Outlook on copper

Recently, Fitch Solutions’ Business Monitor International changed its outlook on copper: the red metal average price might rise to 9,650 dollars per tonne, according to analysts, whereas previous forecasts were more cautious and conservative: 9,500 dollars per tonne. Last October the commodity was traded at 10,000 dollars or above; and averaged 9,609 dollars per tonne, until then. The predicted increase is due to a number of reasons, among which experts mentioned the long-awaited US interest rate cut by the Federal Reserve, expected to trigger investments and therefore create «a tailwind for industrial metals». Geopolitical factors are nevertheless to be taken into account, since «the US-China confrontations», especially, could instead «cap further gains through 2026». As for China itself, the country is still a voracious consumer of copper, whose usage is driven nowadays by green energy, most of all. Fitch Solutions’ BMI reported that solar capacity alone «surged by 212 GW in the first half of 2025» and EV sales are rocketing too: +33% (5.4 million units) over the first two quarters of the year. The demand for copper, destined to renewable energy-related technologies, has caused the Shanghai Future Exchange inventories to hit a 26,800 tonnes-low at the end of September, down from the 160,800 tonnes of material recorded last March.

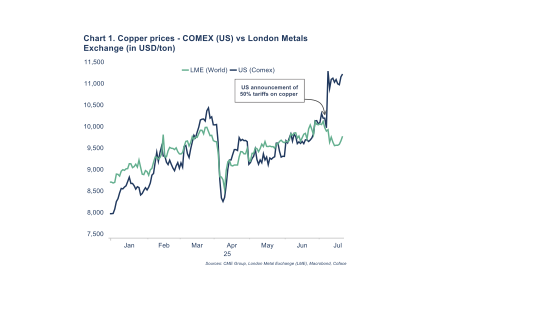

US tariffs announcement caused a 13% increase in Comex copper futures, that jumped last July to 11,290 dollars per tonne (Source: Coface)

Go west

At the same time, LME stocks are also decreasing to some 140,000 tonnes, since large amounts of copper were exported to the United States, due to the decision to increase stocks in order to anticipate the introduction of duty tariffs and to minimise their possible impact. In fact, Comex – the New York Commodity Exchange – stocks were reportedly as high as 329,000 tonnes, last October. Earlier this year ING provided an in-depth analysis on the actual benefits of a 50% sectoral tariff on copper for the US domestic production. Their announcement, as previously reported, caused a 13% increase in Comex copper futures, that jumped last July to 11,290 dollars per tonne. Given that, as ING observed in a dedicated post, the aim is that to encourage new mining projects and support the industry, the initiative might prove unsuccessful. «The US», ING wrote, «produces about 5% of the world’s copper and has seen a 20% decline in production over the last decade. Building new mines in the country can take up to 29 years, due to lengthy permitting processes». Apparently, history taught Trump nothing: tariffs on steel and aluminium achieved no significant result and «in 2024, the output of the US steel industry was 1% lower than it had been in 2017 before the first round of tariffs by Trump, while the aluminium industry produced almost 10% less».

It’s not going to stop

The global financial institution estimates that 850,000 were imported in the United States last year, accounting for 50% of overall consumption, or slightly less: 45%, according to the international risk management company Coface, that also noticed how premiums also underwent a remarkable increase in July (500-1,500 dollars per tonne, as opposite to the 150 dollars average in 2024). Canada, Peru, Mexico and Chile are the main providers and the latter of these, which fulfils 40% of US total request, is facing worrisome criticalities. Fitch Solutions’ BMI has in fact warned that a «wave of supply disruptions» could pose a major threat to global markets. Chilean state-owned miner Codelco experienced a 25% year-on-year decline in output, last August, following a fatal incident occurred at the El Teniente site. Supplies from the Collahuasi mine, among the largest copper reserves in Chile and worldwide, jointly run by Glencore and Anglo-American, also suffered a 27% fall, whereas Teck Resources forecasted volumes from Quebrada Blanca will decrease too. The case of Codelco, in particular, could be a valuable example of how shortsighted US policy-makers are, as Coface pointed out, underlining that the introduction of a 50% duty tariff would give birth to a typical lose-lose situation. «The US represent Chile’s second largest export market, with 28.5% of total copper shipments (…). Codelco is vulnerable to trade barriers and unlike its competitors, operating in multiple regions and sectors, it focuses exclusively on domestic copper production. In 2024 it accounted for a quarter of the country’s copper production and contributed 1.5 billion dollars to the state budget. A potential contraction in US demand in the medium term, in response to tariffs, would reveal particularly damaging to both the company and the Chilean State».

Living for today

Simon Lacoume, sector analyst at Coface, seemed reasonably confident that, thanks to advance purchases, US copper stocks will be rich enough to fulfil the request until the end of this year, since they already amounted to 240,000 tons in July, about 30% of total annual domestic consumption. At the same time the company predicted a slight decline in imports, even though the country’s capacity is not enough to address a growing request for the red metal; but, also, that global oversupply and a sluggish Chinese demand could, at least partially, offset the impact of duty tariffs. On top of that, the economic outlook suggests that the possible price increase should be modest but, in the short run, duty tariffs could hit the building, electric cables and wind turbine producers in first place. Finally, Fitch Solutions’ BMI expects that global refined copper output could rise 2.4% in 2025, largely driven by China, but constrained by limited concentrate availability»; and a «smaller surplus this year, compared with 2024» is also quite likely. On the road ahead, BMI foresees a «significant pipeline of new projects», although rising demand could largely outpace the supply growth.

{kind=link}