The future of batteries lies in next-generation technologies and advanced recycling to reduce cost and material dependency.

The future of electric mobility will increasingly be played out on the terrain of batteries, the element most related to the obstacles that still limit the spread of vehicles, namely cost and range. According to the International Renewable Energy Agency (IRENA), by 2030 the number of electric vehicles on the roads will have to grow from around 44 million in 2023 to 359 million if the climate targets of the Paris Agreement are to be met. This is an unprecedented expansion, which will require five times more batteries to be produced annually than today. Although the planned production capacity seems sufficient – 7,300 GWh of batteries per year against an estimated demand of 4,300 GWh – the real issue is the supply of raw materials in the short term, i.e. by 2030. While IRENA does not see any supply problems in the long term, where recycling will also play an important role, for some minerals there could be bottlenecks by 2030. We are talking about lithium, cobalt, graphite, nickel, copper and manganese, which form the basis of battery chemistry.

Reduction in the use of critical materials

The good news is that technological innovation is already changing the game. According to IRENA, almost 50% of electric cars sold in 2023 used batteries that did not require cobalt or nickel, thanks to the spread of alternative chemistries such as LFP (lithium-iron-phosphate) and LMFP (lithium-manganese-iron-phosphate).

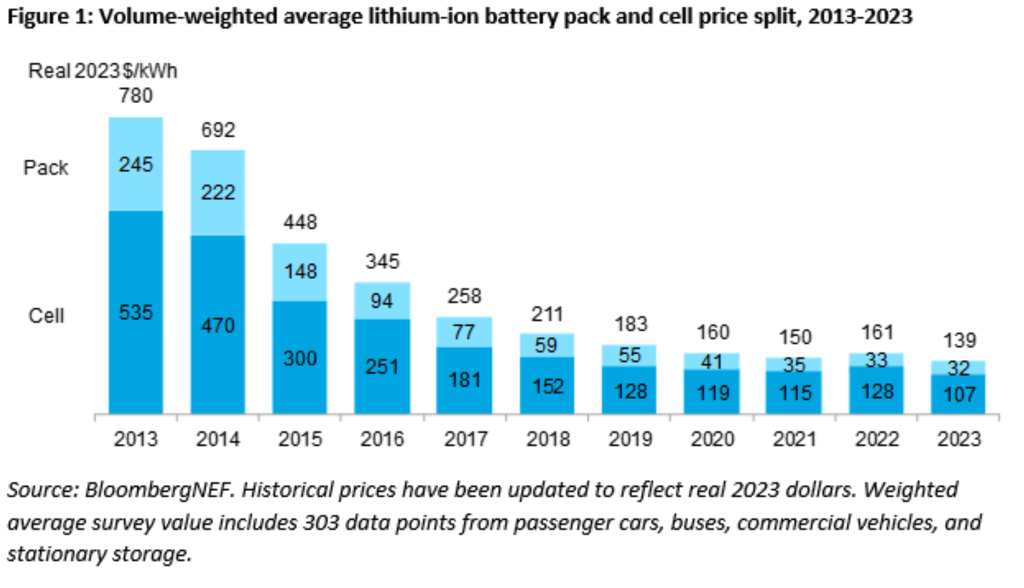

These innovations not only reduce the need for critical materials, but also improve energy efficiency. The energy density of cells, for example, has increased by 30% in the last decade, while that of battery packs has increased by 60%. And this at a cost that for lithium-ion batteries has become about one fifth of what it was ten years ago (figure 1).

Sodium ion batteries: a new frontier

Emerging technologies include sodium-ion batteries. Out of the battery types that exist today, sodium ion batteries represent one of the most promising innovations in the field of energy storage. They are the ones that require the least amount of critical metals and are based on a mineral – sodium – that is widely found in various parts of the earth: it is about a thousand times more abundant than lithium in the earth’s crust. Moreover, it is a technology that also offers good levels of thermal safety. Cheaper, safer and based on abundant raw materials, these batteries offer a promising solution especially for low-cost vehicles and stationary storage. They could help reduce the supply risks and cost volatility that affect critical raw materials today. In terms of construction, sodium ion batteries use hard carbon as an anode material, replacing graphite. This technological choice could not only lower the demand for graphite, but also encourage the use of materials from biogenic sources, reducing the environmental impact.

In general, they offer several competitive advantages: lower costs, higher operational safety, better behaviour at high and low temperatures and better overall thermal stability. Construction of the first plants dedicated to the commercial production of sodium-ion batteries began in 2024, marking an acceleration in the deployment of this technology. Finally, this technology promises to contribute decisively to alleviating bottlenecks in the supply chains of critical materials, thus accelerating the global energy transition.

The Chinese Revolution?

Despite the advantages, up to now, sodium-ion batteries have been attributed a lower energy density than lithium-ion batteries, which is why they were considered suitable for stationary energy storage and electric vehicles that do not require high energy densities, such as city cars or light fleets. However, at the end of April 2025, CATL, the world’s largest battery manufacturer, announced the start of mass production of its sodium-ion batteries by December this year. These new batteries will be destined for a wide range of applications in China, from light electric vehicles to commercial vehicles.

From a technical point of view, the product has some interesting features: the battery achieves a gravimetric energy density of 175 Wh/kg, the highest value achieved to date for sodium-ion batteries. By comparison, current LFP (lithium-iron-phosphate) batteries are in the range of 150 to 200 Wh/kg, which means that sodium-ion technology has already almost reached the level of LFP in terms of density.

According to data released by CATL, these new batteries will be able to guarantee:

- A range of over 200 km in electric mode for plug-in hybrid vehicles.

- Over 500 km of autonomy for fully electric vehicles.

- A service life of 10,000 charge-discharge cycles.

In addition, sodium ion batteries are characterised by outstanding performance to extreme temperatures and maintain full operational capacity down to -40 °C.

Questions remain as to the actual costs and expected production capacity for this new technology. At present, CATL has not yet provided specific details. According to preliminary assessments, sodium-ion batteries could eventually cover a significant share of the market currently occupied by LFP batteries, potentially up to 50 per cent – a prediction that, if it comes true, could reshape the landscape of electric mobility.

In a context of increasing focus on sustainability and strong pressure on critical materials such as lithium, sodium ion chemistry could prove to be a strategic solution: cheaper, safer, and better suited to support widespread and resilient electrification (figure 2).

The economic and supply challenge in EV battery recycling

As the global fleet of electric vehicles continues to grow, the demand for batteries for their production will increase, which will then depend critically on the free availability of key metals and minerals. According to Zhao and colleagues in an article that recently appeared in the scientific journal Geosystems and Geoenvironment, lithium-ion battery production consumed 35 % of lithium and 25 % of cobalt produced globally in 2022. In this context, recycling becomes relevant if one considers that while one tonne of virgin lithium requires about 250 tonnes of spodumene ore or 750 tonnes of mineral-rich brine to be extracted, the same amount of lithium can be obtained from only 28 tonnes of spent lithium-ion batteries. This shows how recycling can become a mainstay of the European automotive industry, reducing dependence on imports of critical raw materials.

However, in addition to technical and regulatory difficulties, the recycling of electric vehicle batteries faces a major economic challenge: the constant change in their chemical composition. NMC and LFP lithium-ion batteries are the most popular today, but the market trend is to reduce the use of expensive and critical materials such as cobalt, preferring nickel and changing the proportions in NMC cathodes (from the NMC111 type a few years ago to the current NMC811). This evolution has reduced the recyclable value of the materials. LFP batteries, now growing strongly (40% of the EV market in 2023, according to the IEA), have an even more fragile value, being based almost exclusively on lithium.

The progressive spread of LFP batteries and the lowering of valuable material content make it more difficult to ensure the profitability of recycling processes. Today, techniques such as hydrometallurgical recycling seem to offer more flexibility than pyrometallurgical recycling and are more suited to a rapidly changing market.

Added to this challenge is that of supply. The availability of spent EV batteries is still limited, as most electric vehicles on the road use batteries that are still operational. Moreover, many disused batteries are exported to Asian countries, complicating the organisation of a local recycling chain

Currently, more than 80% of the world’s lithium-ion battery recycling takes place in China, Korea and Japan, with inputs coming largely from production waste. The expansion of the battery market, also fuelled by new manufacturers with high rejection rates (up to 50%), is increasing the availability of recyclable material, but it will still take several years before the flow of end-of-life batteries becomes constant and sufficient to sustain the growth of the recycling industry.

(Source and Permission: BloombergNEF (BNEF))

IRENA (2024), Critical materials: Batteries for electric vehicles, International Renewable Energy Agency, Abu Dhabi.

CATL: Naxtra Battery Breakthrough & Dual-Power Architecture: CATL Pioneers the Multi-Power Era – https://www.catl.com/en/news/6401.html (accessed 27 April 2025)

Yanyan Zhao, Gurpreet Kaur: ‘The future of recycling for critical metals: The example of EV batteries’. Geosystems and Geoenvironment, Volume 4, Issue 2, 2025, 100376, ISSN 2772-8838,

“Sodium ion batteries – The low-cost future of energy storage?” (2024) by Dr Billy Wu, Imperial College London https://www.youtube.com/watch?v=O3jjJb-CcCU

by Mina Piloni

{kind=link}